Tiger Brokers + Avenir Partnership - An Explanation For Many Things

While already a deeply undervalued stock, now it has a prime catalyst to let it loose

What Everyone Thinks Is Happening

The consensus view on Tiger Brokers is simple: cheap Chinese ADR retail broker (now $7, 9x PE etc), discount to FUTU, no buybacks, no IR activity, China risk, avoid!

This view is wrong.

The market is looking at Tiger’s retail brokerage metrics and drawing conclusions about a company that quietly stopped being a ‘retail’ broker a year ago.

Based on everything I currently know about this company that is publicly accessible, I strongly believe TIGR is worth $30-40 per share by 2027

The current business alone has an intrinsic value of around ~$30, excluding this partnership (which I will get into in a second) which will further boost revenues and AUM, and of course bring much-needed attention to the stock.

If you haven’t yet read the original thesis of why this is the case, check out this.

Why This Tiger Is About To Roar - A Growth Play Mispriced & Misunderstood

Tiger Brokers, trading as Up Fintech Limited ($TIGR) is barely talked about, yet is significantly undervalued in relation to it’s peers. The current price is sitting at $9.2, yet is easily worth $18+.

What Is Actually Happening

Tiger Brokers has been transforming itself into an institutional prime broker and crypto-TradFi bridge - the regulated NASDAQ-listed vehicle through which Asia’s most ambitious digital asset operation accesses traditional financial markets.

The architect of this transformation is Li Lin (Sometimes referred to as Leon Li)

Li Lin founded Huobi (the 9th largest crypto exchange) in 2013 and sold it at the right time with his reputation intact and over a billion in capital.

He recently founded Avenir Group:

SOURCE (along with most others here): https://avenirx.com/

Avenir is not a passive investment group. It is a sophisticated institutional operation comprising:

$907M in BlackRock IBIT - Asia’s largest institutional Bitcoin ETF holder for 7 consecutive quarters, and the 6th largest holder in the world, alongside Jane Street etc:

Bloomberg This is just what we know, due to 13F filings, which do not include ordinary crypto, international positions, etc…

DeepTrading - a proprietary HFT operation with quants running systematic crypto strategies 24/7

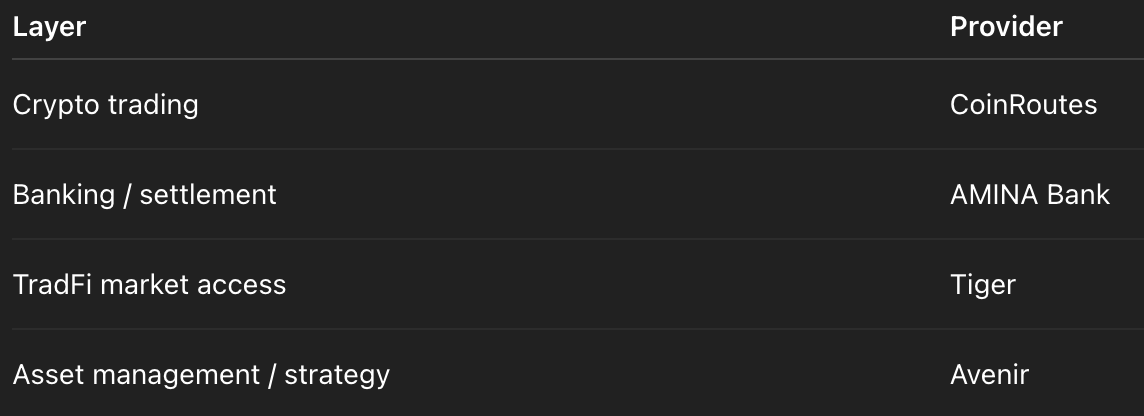

CoinRoutes - institutional smart order routing across 60+ exchanges processing ~$40B monthly, in which Avenir just made a strategic investment/partnership with (February 23, 2026)

Metalpha (NASDAQ: MATH) - blockchain and trading technology solutions, in which Avenir has strategic stake

SINOHOPE - digital asset custody and management

AMINA - Swiss/Global Crypto Bank that just opened in HK.

A ~200-500 person team across Hong Kong, Japan, Singapore, UK, and San Francisco - currently hiring ~30 jobs, mainly Quants/Techies.

This is a prop trading firm, market maker, investor, incubator, and infrastructure builder - running HFT strategies, statistical arbitrage, crypto-TradFi basis trades, and building the PayFi settlement rails that Li Lin believes will replace SWIFT for digital asset transactions.

And Tiger Brokers is their regulated TradFi backbone.

The Partnership: Already Operational

On February 11 2026, at Consensus Hong Kong, Avenir hosted a panel with representatives from Tiger Brokers, CoinRoutes, and AMINA Bank (a Swiss regulated crypto bank). The panel discussed institutional trading infrastructure, cross-asset access, capital efficiency, and settlement design.

After the panel, MOUs were signed with both Tiger Brokers and AMINA Bank. And yes, MOU’s are non-binding and can go nowhere, but read ahead:

Felix from Tiger said on the panel, before the MOU was even signed publicly:

“We worked closely with Avenir. We WILL be the prime broker for Avenir & their customers/clients [meaning their partnership/investment companies, like AMINA/Coinroutes/Metalpha, & Avenir’s own DeepTrading arm].

“In the meantime, we are providing some of the technology that backs the whole infrastructure of Avenir’s project.”

He also said “I do look forward to Avenir offering an all in one experience to the customer to solve the issue”

“We think the whole market is underserved - high expectations on the project and the deliverables at the end.”

The panel ends with Jacob Zhang of Avenir saying “We have something amazing for you coming, so stay tuned”.

(Full video on Consensus HK site)

Already present tense - Operational.

This explains why Avenir has invested in Tiger since early 2025.

CoinRoute’s CEO Ian Weisberger commented on their specific partnership with Avenir: “It’s been a long time in the making. Excited for what we will build together.”

Why Tiger Specifically

Tiger is already built, already listed, already regulated, already operational with $61B in client AUM, and has built institutional client trust. It has the HK SFC license stack Li Lin needs - including a VATP (virtual asset trading platform) license via its YAX subsidiary (which it just so happened to get into when Avenir became an investor), Type 9 asset management, and a full suite of securities and futures licenses.

YAX is “a premier cryptocurrency exchange platform designed to simplify access and valuation of digital assets for its users.”

Tiger also operates in both the USA and Oceania/Asia, linking the Western world to the East, of which Avenir and its clients/customers/partners operate in BOTH areas. Further, Tiger is one of only 12 licensed virtual asset trading platforms in Hong Kong, and likely the main one with ties globally, besides FUTU (who owns PantherTrade).

FUTU at $20B market cap was the obvious alternative, but it’s too large, too entrenched, and too institutionally owned for Li Lin to move fast with. Tiger at $1.4B, with a CEO holding 49% voting control who shares the vision, is the perfect vehicle.

What Avenir Likely Needs Tiger For

Avenir runs sophisticated crypto-TradFi arbitrage strategies, among other prop trading strategies. When Bitcoin ETFs (like IBIT) trade at a premium or discount to Bitcoin spot, that’s an arbitrage opportunity - but only if you can access BOTH sides simultaneously.

Avenir accesses the crypto side via CoinRoutes (60+ exchanges, smart order routing) and others.

Avenir needs to access the TradFi side - IBIT, CME Bitcoin futures, crypto company stocks, ETFs, commodities.

And Avenir’s volume is not small. CoinRoutes alone processes $40B+ monthly. DeepTrading (Avenir’s trading arm) runs HFT strategies. Multiple trading groups operate simultaneously. The 13F filings only show long US equity positions - the prop trading, derivatives, and short-term positions are completely invisible to outside observers, likely representing the majority of actual activity.

The Business Model Shift

Tiger stopped trying to compete with FUTU for typical retail customers, as their primary business, approximately a year ago.

The retail broker model requires:

Expensive customer acquisition ($300-500 per funded account)

Racing to zero on commissions

Competing on marketing spend

Expensive growth

The institutional prime broker model requires:

Zero customer acquisition cost

Flow comes through partnerships

Earn fees on every transaction

Scales infinitely as Avenir grows.

And is much less cyclical than pure retail trading.

This also explains why tiger have leaned so heavily into asset management, wealth management, Investment banking/IPOs, and UHNW/HNW clients.

This is like the Goldman Sachs Prime Services model. Goldman doesn’t advertise to retail investors. Goldman earns fees on institutional flow. It seems to me that Tiger is looking to become “A modern-day Investment Bank”

My interpretation of the stack laid out on the Consensus panel - sounded like this was the setup Avenir was looking for LONG TERM.

Tiger also likely is looking link banking into their app, which COULD happen with AMINA. Similar to FUTU recently partnering/acquiring Airstar bank in HK.

There was also 36 applicants for Stablecoin licenses in HK, of which the first are known from 24th March onwards. It will be interesting to see if AMINA/Tiger applied.

The $580M Cash Pile

“Why no buybacks? Why no dividends? Why is $580M just sitting there, when the company is only $1.4B, with share price lagging?” And largely, why did they raise equity in late 2024, when they were profitable, and seemingly for little reason…

Formal partnership with Avenir likely requires a large investment deployed from Tiger’s balance sheet into Avenir equity, as is typically common in these scenarios. Simultaneously, Avenir is likely to increase its Tiger stake from 6% to a much larger stake. The cross-ownership permanently aligns incentives - neither party can exit without destroying their own investment.

Coinroute’s announced their Avenir investment/partnership just 2 weeks after the panel on Feb 11…

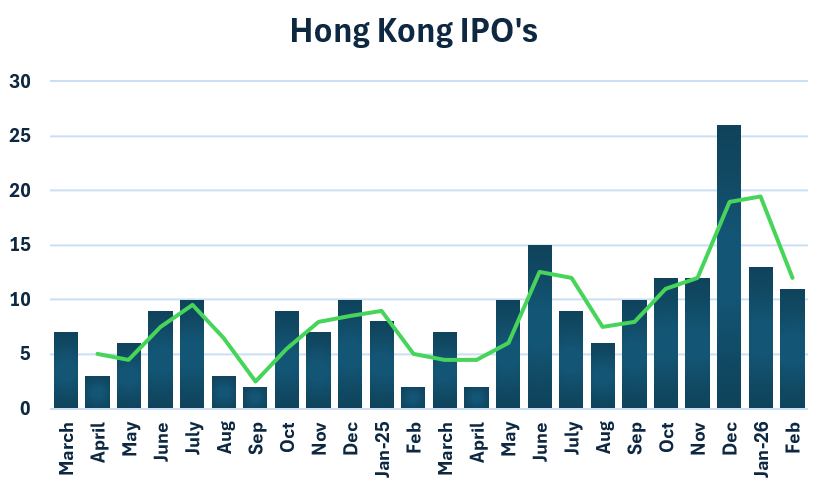

This also explains the Tiger CEO saying in June 2025, “100M investment in HK infra/staff, among other areas, over the next 2 years - doubling headcount” This was it, along with leaning into the booming HK IPO market via Investment Banking services + IPO subscription. (Note that would be [mainly] in CAPEX/OPEX, not from the balance sheet cash).

The ‘Insider’ Accumulation

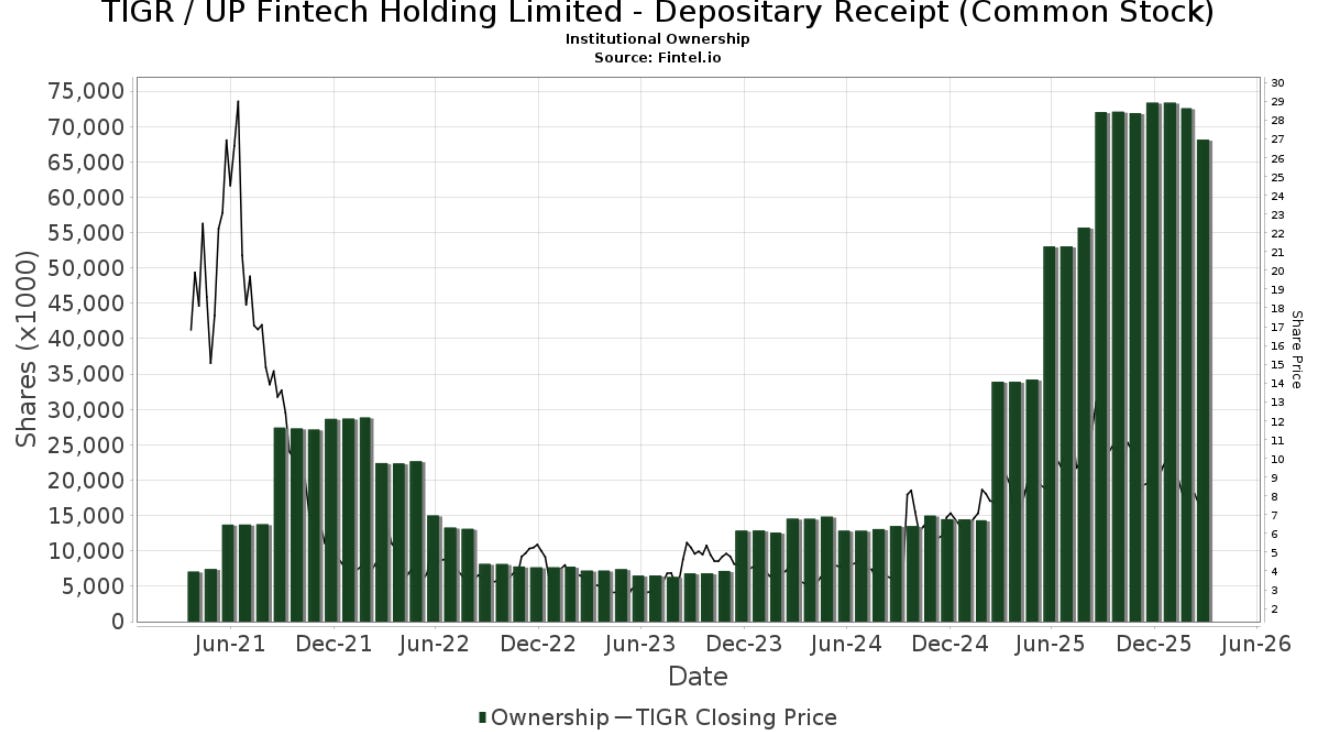

The 13F history for Tiger Brokers shows something interesting: in a stock this cheap, only two outside investors have ever built significant positions.

Li Lin/Avenir Tech Ltd: ~6% - Started accumulating Q1 2025, exactly when private discussions with Tiger were advancing. Held through all volatility. Never sold. The MOU was announced over 1 year after accumulation began. He was not investing in a broker - he was positioning himself before announcing his own plan.

Alon Gonen/Sparta 24 Ltd: ~3% - Founder of Plus500, one of the most successful online trading brokerages ever built. Initiated position Q2 2024. Grew from 4.2% to 61% of his entire investment portfolio at peak concentration - an extraordinary level of conviction from a man who understands online brokerage better than almost anyone alive.

His normal hold period is ~6 months with exits after 50-100% gains. He has held Tiger for nearly two years through gains and losses without following his own playbook.

He appears to trim year-end (both 2024 Q4 and 2025 Q4), possibly for liquidity/tax, and immediately rebuilds, as he knows when the catalyst is coming, so he is not worried about short-term price movements, and knows his own selling provides downward pressure on an already low volume stock…

While his position may have started as a simple investment, it is evident that someone of his nature would have figured out or heard of the Avenir situation early on.

CEO/Founder/Chair Tianhua Wu: ~20% equity, 49% voting rights - Has never appeared on CNBC. Never done a buyback. Never done a dividend. But this is not a CEO who doesn’t care about shareholders. This is a CEO executing a multi-year plan he legally (likely) cannot discuss publicly, or thinks it is not prudent to do so, yet.

Three people. 1/3 of the company already.

Current Revenue Transformation From Retail to IB

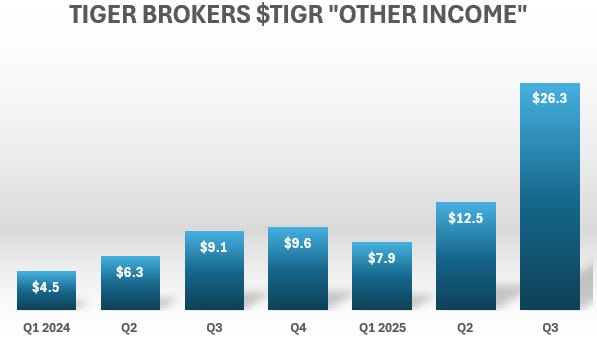

Tiger reports an “other revenues” line covering IB underwriting, IPO subscription, and ESOP SaaS. This jumped over 100% in Q3 alone.

The Q3 2025 jump coincides exactly with Tiger becoming the sole bookrunner on 5 US IPOs, including the largest US-listed Chinese IPO of the quarter, and continued getting on more HK IPO’s. As shown above too, the HK IPO market is booming.

In a recent conference, COO of Tiger said “Wang Shan expressed confidence that it would not be poor [the HK IPO market], as she anticipated that many high-quality companies would be approved for listing in Hong Kong, although valuations are expected to become more reasonable.”

Employee costs jumped simultaneously from $35M to $47M quarterly - they hired the team to execute this vision.

A typical SaaS Fintech broker for retail does not need to have that large of a jump in employee costs, when everything is already in place.

When Q4 prints on March 19, 2026, “other revenues” at (likely) 20%+ of total revenue forces analyst reclassification from retail broker to diversified financial institution.

The Valuation Gap Is Absurd

FUTU Holdings manages $160B AUM and trades at ~13% of AUM - $20B market cap.

Tiger Brokers manages $61B AUM and trades at ~2% of AUM - $1.4B market cap.

Robinhood trades at 35-50x earnings as a pure retail broker with no IB division, no institutional clients, no crypto-TradFi bridge, no Li Lin network. Tiger trades at 9x earnings with all of those things.

Whichever way you assume future figures on a DCF, Tiger comes out to at least $25+.

The Catalyst Stack

March 19, 2026 - Q4 Earnings: Expected beat - considering the analyst estimates are well below their Q3 actual earnings...

Watch “other revenues” growth

Interesting to watch potential questions from analysts on the MOU, if they even took notice...

Stock SHOULD naturally re-rate a bit. Maybe not though, judging by how the stock is currently acting.

‘Mid’ 2026? - Formal Cross-Investment Announcement: Formal partnership revealed publicly. Stock would re-rate quickly.

While it could be coming in later 2026, or even 2027, I assume, based on the fact they ‘floated’ the idea publicly at Consensus HK on Feb 11 2026, after working on it for over a year (likely), that they announce relatively soon.

Tiger is not like Robinhood, constantly telling about their big plans for the future - they just execute, and once its ready they show the world - no hype.

Analyst PT’s:

Goldman is the only firm with a sell rating on TIGR.

They already flipped FUTU from sell to buy. Other anlayst PT’s should come in with news and liquidity and volume rises.

Institutional buying floods in. Drives people to the stock via hype of announcement/new web3 tech, but they find the underlying fundamentals and realize they are excellent.

Long term flywheel:

Once Li Lin billionaire network starts to use Tiger + Avenir grows and acquires/partners with more companies, routing more funds through Tiger.

Tiger gets discovered and builds more trust/credibility, more AUM etc.

As we know from late 2024, tiger is super illiquid, and when there’s some news, it pops hard, >250% in fact last time, in 1 month…

Due to the tightly held float now, I assume it can move VERY quickly once some volume comes in. (Institutions hold around 47% of the float, along with the large insider stake.)

Conclusion

Macro deterioration could hurt sentiment. BTC could fall further. Avenir cross-investment terms could stall or fall apart completely. Timeline could extend beyond 2026.

These risks deserve respect, but I believe this is a very compelling case based on facts/figures, and some intuition/assumptions on timeline, etc.

(I have written this up quickly, without referencing much, so if you want to dive further into something, just ask for the link.)

Even if it doesn’t play out, Tiger is still extremely undervalued. The margin of safety here at 7$ is huge. I won’t get into the valuation gap here, as I cover it deeply in the other article & many of you are already aware.

If you have any thoughts, additions, or criticisms, do let me know. At the end of the day, I am just an outsider trying to piece together what is going on inside the company.

It’s also entirely possible the partnership does eventuate, but does not result in a material change in revenue/profits.

Even if it only alters their revenue to a smaller degree, all Tiger really needs is attention to rerate from it’s current low levels.

If you want to keep up to date with what is going on here, check out my X:

very nice post (but I am baised as a $TIGR bagholder)

Two minor points:

1) IBKR also bought a big stake in TIGR many years ago

2) TIGR actually did buybacks once a few years back

I appreciate needing a warchest in this business but when you are earning $1 to $1.20 per share, have $3 of net cash and are trading at $7 not even having the option of doing a buyback is starting to get pretty silly

5-7x PE multiple

4x EPS to EV multiple